Quantitative Stock Selection Strategy Based on Multi-Scale Transformer

This project proposes a quantitative stock selection strategy based on Multi-Scale Transformer, aiming to mine non-linear Alpha factors in the A-share market through deep learning models.

The strategy combines traditional volume-price factors (Alpha 101) with modern attention mechanisms, enabling it to capture both long-term and short-term price fluctuation patterns in complex market environments.

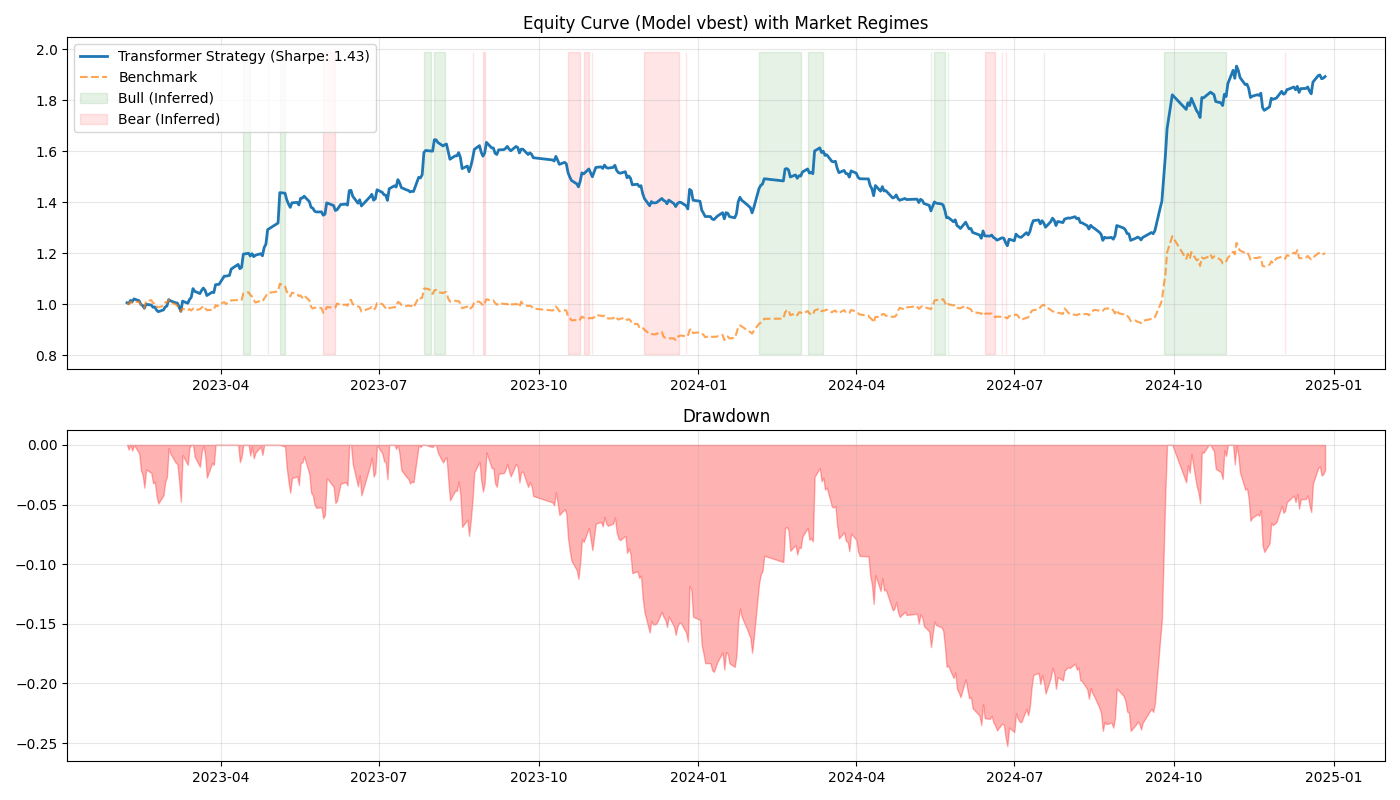

Performance Overview

Figure 1: Equity Curve (Model vbest) with Market Regimes

Figure 1: Equity Curve (Model vbest) with Market Regimes

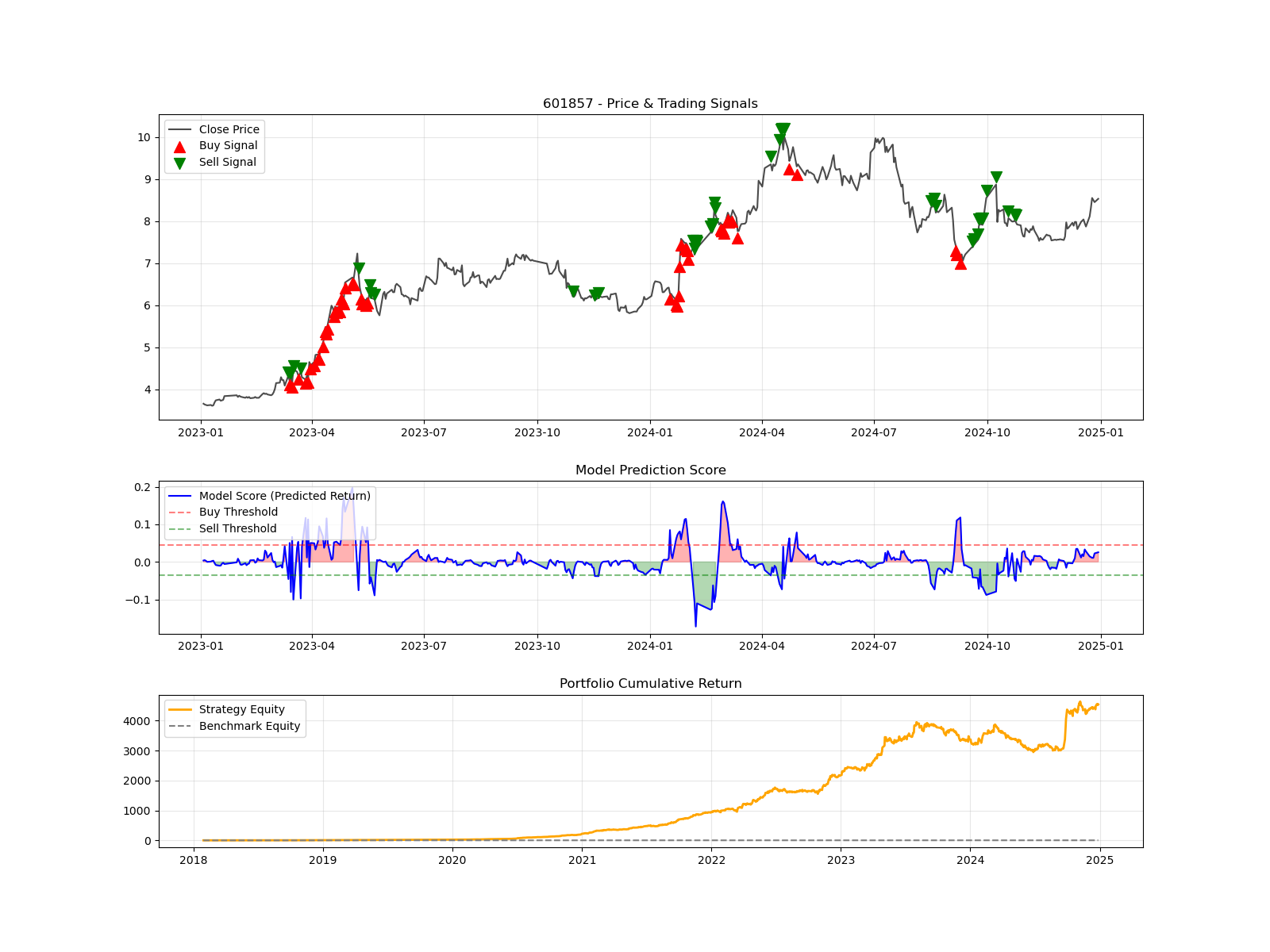

1. Trading Signal Analysis (601857)

Detailed view of model signals on the best performing asset.

Figure 2: Price & Trading Signals (Stock 601857)

Figure 2: Price & Trading Signals (Stock 601857)

2. Key Performance Metrics

| Metric | Strategy | Benchmark |

|---|---|---|

| Total Return | 89.34% | 20.08% |

| Annualized Return | 41.55% | 10.47% |

| Annualized Volatility | 0.2512 | 0.1925 |

| Sharpe Ratio | 1.4275 | 0.5089 |

| Max Drawdown | -25.27% | -20.40% |

| Win Rate | 45.57% | 48.81% |

3. Advanced Risk Metrics

- Sortino Ratio: 3.6661

- Calmar Ratio: 1.6444

- Profit Factor: 1.3209

- Alpha: 0.2916

- Beta: 1.0610

4. Market Regime Analysis (Sub-period)

Performance broken down by inferred market regimes (based on Benchmark behavior).

| Regime | Annualized Return | Sharpe | Win Rate |

|---|---|---|---|

| Bull Market | 243.37% | 5.88 | 50.77% |

| Bear Market | -49.94% | -2.84 | 38.10% |

| Sideways/Volatile | 10.69% | 0.51 | 45.51% |

5. Rank Ability (IC)

- Mean IC: 0.0843

- ICIR: 0.2895

6. Strategy Settings

- Top K: 5

- Position Sizing: Equal Weight

- Stop Loss: -3%

- Transaction Cost: 10 bps